Let me be honest: I used to break a sweat whenever money came up in conversation. Whether my partner blurted out, 'Where did all our money go this month?' or I sat staring at my own dwindling bank account, the discomfort was real. But avoiding financial talk just made things worse—kind of like refusing to open the scary email from your credit card company. In this post, we’ll slice through the taboos and anxieties around money, mix in some surprisingly relatable tales from people who’ve been flat broke (or lost $ in the stock market), and get into the nitty-gritty of what it actually takes to achieve financial independence (and why it’s not all about becoming a hotshot millionaire).

Why We All Freak Out When Money Comes Up (And Why That’s Normal)

Let’s be honest: when you bring up the word money, most of us kind of go blank-faced. Whether it’s with your partner, your boss, your parents, or even just staring at your own bank statement, money talk is universally awkward. If you’ve ever felt your heart rate spike or your palms sweat at the thought of discussing finances, you’re not alone. In fact, there’s a reason why money conversations top the list of “most difficult talks”—right up there with politics and religion.

The Universal Unease: No Situation Is Immune

Money doesn’t care about context. It can make things tense in the boardroom, at the dinner table, or during a quiet moment with yourself. Even people who seem to have it all together financially often struggle to talk about it. Why? Because money is tied to our sense of security, our self-worth, and our dreams for the future. It’s no wonder that, for many, the mere mention of a budget or salary review triggers discomfort or even dread.

How Our Upbringing Wires Us for Money Stress

Our relationship with money is shaped early. I was raised by a single immigrant mother who lived and died a secretary. Every dollar mattered, and financial conversations were often loaded with anxiety. If you grew up hearing “we can’t afford that” or watching adults argue about bills, those experiences can wire you for financial stress later in life. Studies show that children from low-income families have higher resting blood pressure than their middle or upper-income peers—a physical sign of the stress money can cause, even at a young age.

Personal Story: My First Money Fight During a Grocery Run

I’ll never forget my first real money fight. It happened in the most ordinary place: the grocery store. My partner and I were standing in the checkout line, debating whether to splurge on organic produce or stick to the basics. What started as a simple choice turned into a heated argument about spending discipline long-term, priorities, and even our values. The embarrassment of arguing in public was real, but so was the realization: money talks are never just about dollars and cents—they’re about trust, fear, and what we believe is possible for our lives.

‘Survival Mode’ vs. ‘Thriving Mode’: Recognizing the Mental Switch

Many of us operate in “survival mode” when it comes to money. We focus on getting by, paying bills, and avoiding disaster. Shifting to “thriving mode”—where we can think about Financial Independence Early, investing, and building wealth—requires a mental switch. But that’s tough when you’re used to scarcity or financial uncertainty. Even when you start earning more, those old anxieties can linger, making it hard to fully embrace Financial Freedom Steps.

Why Earning More Doesn’t Always Silence the Anxiety

Here’s a secret: financial anxiety doesn’t magically disappear with a bigger paycheck. In fact, many high earners still feel stuck, stressed, or behind. That’s because money issues are often rooted in mindset, not just math. If you’ve ever felt like you’re doing everything right—budgeting, saving, investing—but still can’t shake the stress, you’re experiencing what most people do. Financial independence is as much about emotional freedom as it is about numbers.

The Real Cost of Avoiding Money Conversations

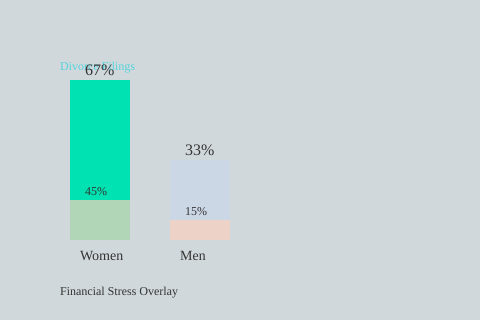

Dodging money talks doesn’t just cost you peace of mind—it can cost you relationships. Financial stress is one of the top causes of divorce. In fact, more than two-thirds of divorce filings are initiated by women, with financial strain often being the tipping point. Avoidance breeds resentment, secrecy, and shame. But here’s the good news: research shows that financially open conversations actually reduce anxiety and help you move from surviving to thriving.

The ‘Sweaty Palms Index’: Measuring Money Talk Anxiety

If there were a “sweaty palms index,” most of us would score high when money comes up. But that’s normal. The key isn’t to eliminate the nerves—it’s to face them, talk openly, and take small, steady steps toward financial independence. Remember, you’re not alone in feeling this way. The journey to financial freedom starts with one honest conversation at a time.

Rethinking Wealth: Why Rich Isn’t Always What You Think

The Myth of the House as a Financial “Must”

For decades, owning a home has been sold as the ultimate sign of financial success. But is it really a must for everyone aiming to achieve financial independence? The truth is, a house can be a great investment—or a money pit. Many people stretch their budgets to buy a home, only to find themselves “house poor,” with little left for savings, travel, or emergencies. Renting, or choosing a smaller or less expensive place, can actually be a smarter move if it keeps your expenses low and your options open. Don’t let social pressure dictate your biggest financial decisions. Sometimes, not buying a home is the best financial independence strategy you can make.

Rich vs. Wealthy: What You See Isn’t What You Get

It’s easy to assume that someone with a big house, fancy car, and a high-powered job is wealthy. But as Scott Galloway says,

“Rich is the things you see, wealth is what you don’t see.”True wealth is about what’s left after the spending stops. It’s about security, freedom, and peace of mind—not just flashy purchases.

Passive Income > Burn Rate: The Real Wealth Benchmark

Here’s the real secret: Passive income generation that exceeds your expenses is the difference between financial freedom and constant stress. If your money works for you—covering your bills and then some—you’re truly wealthy, no matter what your salary says. If you’re spending everything you earn (or more), you’re just one bad break away from trouble, no matter how much you make.

| Person | Annual Income | Taxes/Expenses | Passive Income | Annual Spending | Financial Status |

|---|---|---|---|---|---|

| Investment Banker | $3–10M | 50%+ taxes, high lifestyle costs | Low | Most of income | Unstable, anxious |

| Frugal Dad | $52,000 | Low | $52,000 (pension, social security, laundry machines) | $48,000 | Secure, stress-free |

Real-Life Examples: The Big Earner vs. the Frugal Dad

Scott Galloway tells two stories that flip the script on what it means to be wealthy. First, there’s his friend, a top M&A banker making $3–10 million a year. On paper, he’s the definition of “rich.” But after taxes, alimony, a Hamptons home, and a “master of the universe” lifestyle, he spends almost everything he makes. He hasn’t saved much, and he lies awake at night worrying about what happens if the big paychecks stop. Despite the income, he’s not truly wealthy—he’s trapped by his expenses and lifestyle inflation.

Then there’s Galloway’s father. He’s 94, retired, and lives on a modest $52,000 a year from his Navy pension, Social Security, and the coins he collects from six washer-dryer machines in trailer parks. He spends $48,000 a year—less than he brings in. He’s not flashy, but he’s secure. His passive income covers his needs, and he sleeps well at night. This is the real goal: passive income generation that outpaces your “burn rate.”

Why Economic Pride Can Trap You

Many people fall into the trap of economic pride. You work hard, so you “deserve” the big house, the new car, the luxury vacations. But this mindset can sabotage your path to financial independence. The more you spend to keep up appearances, the less freedom you have. True wealth is about options, not obligations.

Personal Tangent: The Car That Didn’t Fix My Life

I once thought buying a new car would solve my problems. I’d finally feel successful, confident, and happy. Spoiler: it didn’t. The excitement faded fast, but the payments stuck around. It was a lesson in how easy it is to confuse spending with satisfaction. If you want to avoid lifestyle inflation, focus on what truly matters—security, freedom, and peace of mind—not just what looks good on Instagram.

Smart Moves (and Some Mistakes) on the Road to Real Financial Independence

Budgeting Attempts Gone Wrong: Confessions of an App-Abandoner

Let’s be honest: most of us have downloaded at least one budgeting app, filled in a few numbers, and then… never opened it again. You’re not alone. The truth is, building a budget plan that actually sticks is less about the perfect app and more about finding a system you’ll use. If you’re an app-abandoner, try old-school methods: a simple spreadsheet, a whiteboard, or even a notebook. The key is tracking what you spend and what you save—consistently. If you can automate your savings, even better. Automatic deposits savings take the willpower out of the equation, making progress toward Financial Independence Retire Early (FIRE) almost effortless.

Why Investing Early (Even a Little Bit) Beats Fast Cars and Big TVs

It’s tempting to upgrade your lifestyle with every raise—maybe a bigger TV, a flashier car, or a larger apartment. But here’s the catch: the earlier you start saving and investing, the more you benefit from the compound growth power. Even small amounts make a huge difference. Consider this:

| Monthly Savings | Start Age | Value at 65 (7% annual return) |

|---|---|---|

| $300 | 25 | $762,000 |

| $600 | 35 | $684,000 |

Starting at 25 with $300/month beats starting at 35 with $600/month. That’s the magic of compound growth. The earlier you start, the less you need to save to reach your goals.

The Surprising Impact of Lifestyle Inflation—And How to Dodge It

Lifestyle inflation is sneaky. As your income rises, so do your expenses—unless you’re vigilant. Maybe you know someone who “needs” a million dollars a year to live in a trendy city, but could live just as well (or better) elsewhere for less. The lesson? Control your burn rate. Moving to a lower-cost area, resisting the urge to upgrade everything, and focusing on what truly makes you happy can take a world of stress off your shoulders. Remember: Wealth is passive income greater than your burn.

The 25x Rule: What It Is and Why It’s a Game-Changer

Here’s a simple, powerful rule for Financial Independence 2025 and beyond: accumulate 25 times your annual expenses. This is known as the 25x Rule. If you spend $40,000 a year, you’ll need $1,000,000 invested to retire early and safely withdraw 3-4% per year. This rule gives you a clear target—no guesswork, just math.

| Annual Expenses | 25x Rule Target |

|---|---|

| $30,000 | $750,000 |

| $50,000 | $1,250,000 |

Personal Anecdote: The Year I Saved $300 a Month and Actually Saw It Pile Up

Back in college, I had to save $3,000 over the summer or I wasn’t going back for my senior year. I survived on $78 a week—including rent. It was tough, but seeing those savings grow was addictive. That year, I learned that gamifying saving money—making it a challenge—can make all the difference.

Wild Card: The 'Gamified' Savings Contest—Real Friends, Whiteboards, Pepperoni Pizza, and a 12-Week Challenge

One summer, my friends and I turned saving into a game. We tracked every dollar on a whiteboard, met up for pizza, and competed to see who could save the most in 12 weeks. The result? We all saved more than we thought possible. As the transcript says:

“Gamify saving money with a partner...God, that’s powerful.”

Whether it’s a partner or a group of friends, a little friendly competition—and total transparency—can supercharge your savings.

Tables Turn: How Lifestyle Choices Change Everything

Relocating to Reduce Burn Rate: Real-World Examples

One of the biggest myths in the journey to financial independence is that you need to keep earning more, always chasing the next raise or promotion. But what if the real power lies in controlling your expenses—your “burn rate”—instead? Let’s look at two real-life stories that show how changing where and how you live can completely flip your financial script.

- San Jose to Costa Rica: A couple in their late 50s, living in San Jose, realized that their current lifestyle would not be sustainable in retirement. Despite years of hard work, their passive income wouldn’t cover their expenses. The solution? Consider a dramatic lifestyle shift: “Why wouldn't you try and cut your burn 40% and move to Costa Rica?” By relocating, they could sell their high-priced home, slash their cost of living, and finally achieve the financial security they’d been chasing for decades.

- NYC to Portugal: Another example comes from a friend who ran a hedge fund in New York City. Living in TriBeCa with three kids, he needed a staggering $1 million a year just to maintain his lifestyle. After moving to Portugal, his family enjoys a beautiful home, great food, and excellent education—all for $400,000 a year. That’s a 60% reduction in annual expenses, with a major boost in quality of life.

Comparing Cost of Living, Stress, and Quality of Life

These stories highlight a key lesson: Reducing expenses has a bigger impact on wealth and happiness than chasing raises alone. When you avoid lifestyle inflation and focus on living below your means, you gain flexibility and peace of mind. Here’s how the numbers and the feelings stack up:

- Cost of Living: Both families slashed their annual expenses by 40-60% simply by relocating. This is the ultimate Expense Tracking Budget hack—move somewhere your money stretches further.

- Stress: Lower expenses mean less pressure to earn more. This reduces financial anxiety and the constant fear of “not having enough.”

- Quality of Life: With less financial stress, relationships often improve. There’s more time for family, hobbies, and health. Both case studies reported happier marriages and better work-life balance after their moves.

The Power of Controlling 'Burn' vs. Chasing Higher Income

It’s tempting to think the answer is always “make more money.” But every dollar you don’t have to spend is a dollar you don’t have to earn. This is where Net Worth Benchmark thinking comes in: focus on what you keep, not just what you make. Building a Build Budget Plan around your real needs—rather than your zip code’s expectations—can change everything.

Unexpected Side Effects: Happier Relationships, Lower Stress, Better Health

When you cut your burn and simplify your life, the benefits go way beyond your bank account. Less stress means better sleep, improved health, and more time for the people and activities that matter most. Many people find that downsizing or relocating actually brings them closer together as a family, rather than feeling like a sacrifice.

Quick Tangent: The Guilt and Pride Clash

Let’s be honest: making a big financial “detour” can trigger some serious emotions. There’s often guilt about leaving behind a familiar place or pride tied to a fancy address. But remember, downsizing or relocating isn’t a failure—it’s a strategy. Dozens of people are happier and wealthier for making these bold moves. Sometimes, “where” you live (and how simply) matters more than “what” you make.

Comparative Summary: Before & After Lifestyle Switches

| Case | Location (Before/After) | Annual Expenses | Stress Level | Quality of Life |

|---|---|---|---|---|

| San Jose Couple | San Jose / Costa Rica | 100% / 60% (cut by 40%) | High / Low | Worried / Secure, Happy |

| NYC Hedge Fund Family | NYC / Portugal | $1M / $400K | Very High / Low | Stressed / Thriving |

In the end, the tables really do turn when you take control of your lifestyle. Lifestyle Inflation Avoid isn’t just a catchphrase—it’s the key to unlocking financial independence, no matter your age or income.

Talking About Money: The Unlikely Secret Weapon

Why Most Money Experts (and Regular Folks) Clam Up—And How It Backfires

Let’s be honest: talking about money makes most people squirm. Even financial experts often avoid open conversations about their own financial mistakes or strategies. This silence is costly. When we don’t talk about money, we miss out on learning key financial literacy skills, smart saving habits, and tax efficiency strategies. We also risk repeating the same mistakes as our peers—simply because no one’s willing to admit what went wrong.

Money shame is real. For many, it feels easier to talk about almost anything else. But the truth is, the best way to get better at money is to actually talk about it. Sharing your experiences, both good and bad, helps you build a better budget plan and develop financially independent habits.

Being Vulnerable About Financial Flops (It’s More Common Than You Think)

It’s easy to believe you’re the only one who’s ever maxed out a credit card or lost money in the market. But financial flops are universal. When you open up about your own setbacks, you give others permission to do the same. This vulnerability is powerful. It leads to honest discussions about smart saving, investment mistakes, and even tax efficiency strategies you wish you’d known sooner.

For men, this can be especially tough. Many feel pressure to appear financially successful at all times. Admitting to a loss or asking for advice can feel like admitting weakness. But as one expert put it,

“If you want to be good at it, you gotta get literate at it and you want to bring it up with your friends.”

Wild Card: Practice ‘Adulting’—Why We All Need a Class in School for This

Imagine if every high school senior took a class called “Adulting.” Instead of just learning calculus, students would master the basics of financial literacy: how credit cards work, how to build a budget plan, and why tax efficiency strategies matter. The reality? Most young adults can solve complex math problems but don’t understand how interest rates or Roth IRA income limits (for 2025: $165,000 single, $246,000 married filing jointly) affect their real lives. Making financial literacy as essential as any core subject could change everything.

The British ‘Accidentally Rich’ Myth—And How It Shapes Conversation

There’s a cultural myth, especially strong in Britain, that the best kind of wealth is the kind you “accidentally” stumble into. You’re supposed to be so talented that money just happens to you—no effort required. But this myth keeps people from talking about the work, planning, and sometimes the failures that go into building wealth. In reality, financial independence takes intention, learning, and yes, plenty of conversation.

How Sharing Real Numbers With Friends Beats All Other Financial Advice

Here’s the wildest secret: sharing real numbers with friends is more valuable than any book or online course. When you talk openly about your income, savings, and investment strategies, you learn faster and avoid costly mistakes. Experts spend over four hours a week talking to others about their economic well-being—discussing everything from tax loopholes to when to refinance a mortgage. This social approach multiplies knowledge and reduces shame. Maybe it’s time to add “financial group chat” to your to-do list.

Table: Sample Prompts for Opening Up Money Conversations With Family and Friends

| Prompt | Why It Works |

|---|---|

| “How did you learn to budget? Any tips?” | Opens the door to sharing practical budget plan strategies. |

| “What’s one financial mistake you wish you could undo?” | Normalizes talking about financial flops and lessons learned. |

| “Have you found any smart saving hacks lately?” | Encourages sharing of actionable smart saving habits. |

| “Do you know any tax efficiency strategies I should look into?” | Promotes learning about tax advantages together. |

| “Would you ever move for a lower cost of living or better taxes?” | Starts a conversation about lifestyle choices and financial independence. |

Destigmatizing money talk is the unlikely secret weapon for building financially independent habits. The more you talk, the more you learn—and the less you fear.

Skills, Not Just Degrees: Earning Your Way to Independence

Let’s get real: you don’t need a fancy diploma to build financial security. In today’s world, practical skills, curiosity, and the willingness to hustle can open more doors than a degree ever could. If you’ve ever felt stuck because you don’t have the “right” credentials—or you’re holding a degree you no longer care about—take heart. Degrees don’t always guarantee financial success. What matters most is your ability to turn what you know into income, especially if you’re aiming for Financial Independence Early.

Why Skills Trump Diplomas in 2025

It’s 2025. Companies care less about where you went to school and more about what you can actually do. Adaptability, skill stacking, and hands-on results are the new gold standard. The smartest move? Invest in yourself, not just in stocks. Practical, transferable skills—like communication, coding, digital marketing, or project management—are in high demand and can be learned outside a classroom.

Challenging Corporate Myths: The Degree Delusion

There’s a stubborn myth that companies only hire people with degrees. But the truth is, more businesses are ditching degree requirements in favor of real-world skills. They want problem-solvers, not paper credentials. If you can show results—whether through a portfolio, freelance gigs, or side projects—you’re already ahead of the curve.

Degrees don’t always guarantee financial success.

Translating Your Skills into Income Streams

Maybe you’re wondering, “I have skills, but how do I monetize them?” The answer: by connecting your strengths to real-world needs. Here’s how you can start:

- Identify your marketable skills: Think beyond your job title. Are you great at organizing, writing, designing, or fixing things? List out what you’re good at—even hobbies count.

- Research demand: Use platforms like Upwork, Fiverr, or LinkedIn to see what people are paying for. Is there a niche you can fill?

- Start small: Offer your services as a side hustle. Freelance, consult, tutor, or create digital products. The goal is to test the waters and build confidence.

- Stack your skills: Combine two or more abilities (like writing + SEO, or coding + design) to stand out and charge more.

- Automate and scale: Once you’ve got traction, look for ways to generate Passive Income—like online courses, eBooks, or affiliate marketing.

Personal Scenario: What I Learned Moonlighting as a Freelance Writer

When I started moonlighting as a freelance writer, I had no formal journalism degree. My day job paid the bills, but writing on the side taught me more about negotiation, marketing, and client management than any classroom ever could. I learned how to pitch, price my work, and build a portfolio. Eventually, those skills led to Multiple Streams of Income—from blog posts and newsletters to editing gigs and digital products. The best part? I was in control of my time and earnings.

Why Now Is the Best Time to Monetize Your Skills

Technology has leveled the playing field. Whether you’re 18 or 58, you can learn new skills online—often for free. Platforms like YouTube, Coursera, and Skillshare make it easy to pick up everything from coding to copywriting. The gig economy is booming, and remote work is the norm. There’s never been a better moment to turn your abilities into cash flow and work toward Financial Independence Early.

Connecting Your Strengths to Income Streams

Think about how your unique strengths can fuel Passive Income Generation or active side hustles. Are you a natural teacher? Launch a course. Love photography? Sell stock images. Good at organizing? Offer virtual assistant services. The key is to start, experiment, and adapt.

- Saving and Investing: As you earn more, channel those funds into savings and investments. This accelerates your path to independence.

- Keep learning: The more skills you stack, the more opportunities you create for yourself—no degree required.

Remember, practical, transferable skills are your ticket to freedom. It’s never too late to start earning your way to independence—on your own terms.

FAQ: Your Most Uncomfortable (and Useful) Financial Questions

Let’s be honest: money talk can make anyone squirm. Most of us have questions we’re too embarrassed to ask, especially when it comes to financial independence, building an emergency fund, or recovering from mistakes. The truth? No one has it all figured out. So, let’s get candid and tackle the questions you might be afraid to ask but absolutely need answered on your journey to financial freedom.

What if my partner and I can’t agree on spending priorities?

This is more common than you think. Money is emotional, and when two people have different backgrounds or dreams, it’s natural to clash. The first step is to talk openly—without judgment—about what matters most to each of you. Try building a budget plan together, where both partners get a say. Sometimes, leaning into each other’s strengths helps: maybe one of you is great at tracking expenses, while the other is a big-picture planner. Compromise is key, and so is revisiting your plan regularly as life changes.

Is it ever too late to start saving for financial independence?

Absolutely not. It’s never too late to start. Many people worry that if they haven’t saved enough by their 40s or 50s, it’s game over. That’s simply not true. Even if you’re starting later, you can still take meaningful steps toward financial independence. You might need to adjust your expectations or get creative—like downsizing, moving to a lower-cost area, or finding new streams of income. Remember, the goal is progress, not perfection. Every step you take now makes your future more secure.

How much should I have in an emergency fund?

The classic rule of thumb is to save enough to cover three to six months of living expenses. This “emergency fund rainy day” stash is your safety net if you lose your job, face a medical emergency, or have an unexpected expense. If your job is unstable or you have dependents, aim for the higher end. If you’re just starting, don’t get overwhelmed—begin with one month’s expenses and build up from there. The peace of mind is worth it.

Do I need to own a home to become financially free?

No, home ownership is not required for financial independence. Many people assume buying a house is the ultimate step, but it’s not the only path. Renting can offer flexibility and sometimes even save you money, especially if you’re willing to relocate to a lower-cost area. For example, if you’re living in an expensive city like San Jose but dream of financial freedom, consider moving somewhere more affordable—even internationally. The key is to keep your “burn rate” (monthly expenses) low so your savings and passive income go further.

What’s the quickest way to start earning passive income?

There’s no magic bullet, but the fastest way is to leverage what you already have. Do you own a home? Renting out a room or the whole place can generate income. Have skills or hobbies? Turn them into digital products, online courses, or freelance gigs. Investing in index funds or dividend stocks is another classic route, though it takes time to build up. The important thing is to start small and experiment—don’t wait for the “perfect” opportunity.

Can I recover from money mistakes (even big ones)?

Yes, you can. Everyone screws up financially at some point—sometimes more than once. Most people experience at least two major money failures in their lives. Even if you’ve been broke in your 40s (like many, including the author of this guide), it’s possible to bounce back. The key is to face your situation honestly, learn from what happened, and take practical steps to rebuild. Shame is normal, but it doesn’t have to define your future.

In the end, the path to financial independence is rarely smooth. You’ll make mistakes, change directions, and sometimes feel lost. What matters most is that you keep asking questions, keep learning, and keep moving forward. No question is too “dumb” or too late to ask—especially when your financial freedom is on the line.

TL;DR: Money is weird for everyone, but talking openly, building passive income, avoiding lifestyle inflation, and planning smartly are the keys to shaking off stress and achieving authentic financial freedom. Start small, stay curious, and remember—it’s not about being rich, it’s about being free.

Post a Comment