Picture this: waking up in a cramped Mumbai shelter, fast-forwarding to nabbing a seat at MIT, and eventually helming tech teams handling over $60 billion. How? Not luck—and definitely not through tired slogans. I learned, failed, and adapted. Forget sugarcoated advice—here are the true cheat codes I wish I'd known sooner. You might find some oddball insights, a little rebellion against mainstream mantras, and (hopefully) validation that your journey isn't supposed to look like a Hallmark ad. Let's get uncomfortably real about what it takes to win at money, work, and, honestly, life.

Cheat Code #1: The ‘Invest Early or Regret Later’ Rule (The $1.4 Million Math Napkin)

Saving ≠ Investing—Why Waiting Costs Real Money

Let’s get this straight: saving is not investing. Stashing cash in a high-yield savings account might feel responsible, but if you’re not putting your money to work, you’re missing out on the single most powerful force in personal finance—compound interest growth. For Millennials focused on financial planning, understanding this distinction is the first step to building real wealth.

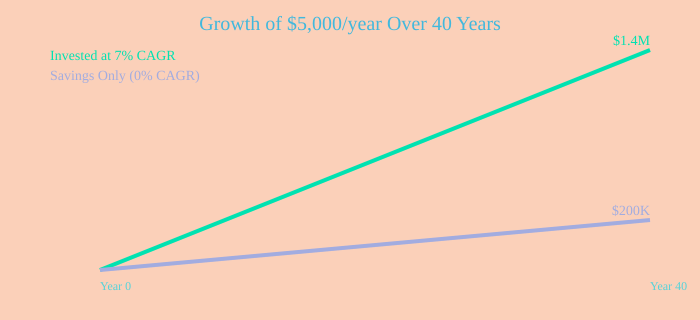

The Power of Starting Early: The $1.4 Million Napkin Math

Investing can seem intimidating. The jargon, the charts, the endless news cycles—it’s easy to feel like you need a finance degree just to get started. But here’s the truth: investing early doesn’t have to be complicated. In fact, the simplest approach often wins.

Here’s the napkin math that could change your life: If you invest just $5,000 per year in a low-cost S&P 500 index fund starting in your 20s, and you keep doing that every year until you retire in your 60s, you could end up with about $1.4 million. That’s assuming a 7% average annual return, which is in line with historical S&P 500 performance after inflation.

Compound Growth: Boring, Predictable, and Magical

This is the magic of compound interest growth. Your money earns returns, those returns earn returns, and over decades, the effect snowballs. It’s not flashy or exciting, but it works—especially when you start investing early and let time do the heavy lifting.

Panic Selling: A True Wealth Killer

Here’s where most people go wrong. When the market drops, panic sets in. I learned this the hard way during the 2008 financial crisis. The S&P 500 dropped almost 50%. I watched my investments lose 30% of their value and, like many others, I panicked and pulled my money out. When the market bounced back a year or two later, I stayed on the sidelines, too scared to jump back in.

If I had done absolutely nothing and stayed in the market, my net worth today would be 40% higher.

This is the cost of emotional investing. Financial planning for Millennials isn’t just about picking the right funds—it’s about having the discipline to stay invested, especially when it feels uncomfortable.

Index Fund Benefits: Why Simple Wins

- Low-cost: Index funds charge minimal fees, so more of your money stays invested.

- Broad-market exposure: You own a slice of hundreds of companies, reducing risk.

- Ideal for Millennials: Perfect for long time horizons and moderate risk tolerance.

Action Step: Automate and Ignore the Drama

The best way to harness compound interest growth is to automate your contributions. Set up automatic transfers to your investment account every month. Don’t chase meme stocks. Don’t try to time the market. Don’t let headlines scare you out of the game. Touch nothing investing—just keep buying, no matter what.

Remember: Start investing early, stay consistent, and let compound growth do the rest.

Cheat Code #2: Passion Doesn’t Pay (But Practiced Skills Will)

Let’s get real: the “follow your passion” advice is one of the most persistent myths in career growth mentorship and financial planning strategies for millennials. You’ve heard it everywhere—do what you love, and the money will follow. But what if I told you that for 96% of people, that’s just not true?

Following Your Passion Doesn’t Work for 96%—Study Backs It Up

A revealing study from a Canadian university found that only 4% of students could actually make money by following their passion. That means 96% of us can’t turn our passion into a real, sustainable career. Think about that for a moment. The odds are stacked against you if you’re betting your financial future on passion alone. This isn’t just theory—it’s cold, hard data that should shape your approach to financial goals as a millennial.

Success Creates Passion, Not the Other Way Around

So, what happened to all those “do what you love” slogans? Here’s the truth: passion doesn’t lead to success; success leads to passion. When you become great at something—when you build valuable, marketable skills—passion tends to follow. You start to love what you’re good at, especially when it pays the bills and opens doors.

By being great at something, passion will follow you.

Anecdote: My First Boston Job—Paid to Learn, Not to Love

Let me share a quick story. My first job in Boston was at a smelly, windowless help desk. It was far from glamorous. But I was paid to learn. I wasn’t passionate about troubleshooting printers or crawling under desks, but I focused on building skills—problem-solving, communication, technical know-how. Those skills became stepping stones for my entire career and financial growth. The magic wasn’t in the passion; it was in the practice and the paycheck.

Hone Marketable Skills—That’s Where the Real Magic Happens

Instead of obsessing over finding your “calling,” obsess over compounding your skills. Ask yourself: What skills can I practice and hone that are monetizable? Whether you’re still in school or stuck in a job that doesn’t excite you, focus on building a toolkit of valuable abilities. This is the foundation of building passion through skill and the backbone of smart financial planning strategies for millennials.

Practice, Not Just Talent, Differentiates Winners

Look at the world’s top performers. Why do Taylor Swift and Kobe Bryant stand out? It’s not just talent—it’s relentless practice. Elite musicians at Berklee College of Music, some of the most gifted people on the planet, still put in 8 to 10 hours of practice every single day. They work on the hard stuff—the scales, the drills, the techniques that make their fingers bleed and their bodies ache. Excellence doesn’t come naturally; it is built through practice.

Banking on talent alone is like having a Ferrari with no engine. Beautiful to look at, but it’s not going anywhere.

Don’t Obsess Over ‘Calling’—Obsess Over Compounding Your Skills

Your “superpower” might be different from mine. For me, it’s the ability to sit still and focus on deep work for hours without distraction. For you, it might be something else entirely. The key is to discover it and invest in continuous self-improvement. Remember, skill development outpaces passion as a driver for both financial and professional success. Each new skill you master increases your value and future returns—this is the true engine of career growth mentorship and financial goals for millennials.

- Don’t chase rainbows—chase skills that pay.

- Practice relentlessly; persistence always pays.

- Let passion catch up to your success, not the other way around.

So, the next time you hear “follow your passion,” remember: build your passion through skill, and let your career—and your bank account—thank you later.

Cheat Code #3: Your Career = An Investment Portfolio (Even When It Stinks at First)

Here’s the truth most career advice skips: Every job, even the ones that feel pointless or soul-crushing, is a chance to bank skills or connections. If you want to master Career Growth Mentorship and ace Financial Planning Millennials style, you need to treat your career like an investment portfolio—not just a paycheck. This mindset shift is the ultimate cheat code for long-term success, even when your early gigs are far from glamorous.

Treat Your Career Like a Diversified Investment Portfolio

Think of your early career as a diversified asset portfolio:

- Skills = Stocks: Each new technical or soft skill you learn is like buying a share in your future. These skills appreciate and compound over time, just like stocks in a well-managed portfolio.

- Connections = Bonds: Every relationship you build is a bond that pays dividends down the line. Networking early can unlock exponential career returns, especially when you least expect it.

Just like in Investment Portfolio Management, diversification is key. Don’t just focus on one area—build a mix of technical skills, soft skills, and professional relationships.

Going ‘Above and Beyond’ in the Grind Pays Off

Let’s get real: your first job probably won’t be glamorous. My own journey started at the absolute bottom. Picture this: a windowless, cramped help desk in a 600-person consulting firm, surrounded by cables, spare parts, and three other employees who, frankly, all smelled bad. We got yelled at a lot. But here’s the kicker—I was having the time of my life.

I was getting paid to learn everything about technology.

I worked 14-15 hour days, took on extra projects, and spent weekends diving into operating systems, networking protocols, and communication skills. I wasn’t just building a resume—I was building a portfolio of skills and connections that would compound in value over time.

Skill Compounding: The Career Growth Mentorship Secret

Just like compound interest grows your wealth, skill compounding accelerates your career growth. In my first five years, I invested over 15,000 hours into learning and networking. That grind period paid off: I earned my first promotion to program manager and finally got my own office. But the real payoff came later.

In less than 20 years from my first promotion, I became the CEO of an epic tech company.

The lesson? Autonomy and glamour come much later. Early on, it’s all about patience, grit, and relentless investment in yourself.

Soft Skills and Technical Skills Both Compound in Value

Don’t just chase technical expertise. Communication, collaboration, and leadership are the “blue-chip stocks” of your career portfolio. These soft skills compound in value and become your differentiators as you climb the ladder. Career Growth Mentorship isn’t just about what you know, but how you connect and lead.

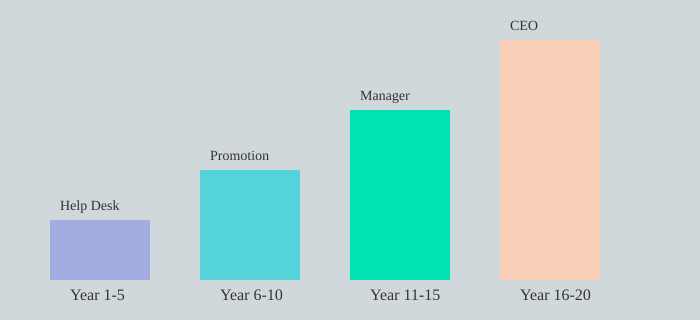

Personal Timeline: From Windowless Help Desk to CEO

Here’s a snapshot of how skill and connection investment compounds over time:

| Years | Role | Skills/Connections Gained | Career Level |

|---|---|---|---|

| 1-5 | Help Desk | Technical skills, basic networking, communication | Entry-Level |

| 6-10 | Program Manager | Project management, leadership, deeper connections | Mid-Level |

| 11-15 | Senior Manager | Advanced leadership, strategic networking | Senior-Level |

| 16-20 | CEO | Vision, executive leadership, industry-wide connections | Executive |

For Financial Planning Millennials, the takeaway is clear: focus on building your long-term skill and connection portfolio, not just short-term perks. Every hour invested in learning and networking is a share in your own future growth.

Cheat Code #4: Emergency Funds, Four-Bucket Budgets, and the Real American Dream

Emergency Savings Fund: Your Non-Negotiable Financial Buffer

If you’re serious about financial resilience, building an emergency savings fund isn’t optional—it’s your first line of defense. Aim for a minimum of three to six months’ worth of living expenses. This buffer is what stands between you and financial disaster when life throws a curveball—like a layoff or a sudden medical crisis.

Consider this: a friend of mine, healthy and in his mid-40s, was driving home when the right side of his face went numb. He pulled over, called 911, and was rushed to the hospital. The diagnosis? A brain tumor. No warning, no preparation. The medical bills were staggering. If he hadn’t had an emergency fund, his family would have faced not just emotional turmoil, but financial ruin. These events don’t schedule themselves—they just happen. And when they do, your emergency fund is your safety net.

FBI Framework: Four Buckets for Financial Clarity

Next, it’s time to form your own FBI—your Financial Bureau of Investigation. The first step: If you don’t know where your money is going, how can you control it? The answer is simple: track, categorize, and optimize your cash flow.

Break your finances into four buckets:

- Emergency: Your savings for a rainy day—your essential safety net.

- Essentials: Regular expenses like rent, utilities, groceries, and transportation.

- Equity: Investments and assets that build your long-term wealth.

- Enjoyment: The fun stuff—vacations, hobbies, entertainment. But here’s the catch: only fund this bucket after the first three are covered.

| Bucket | Purpose | Priority |

|---|---|---|

| Emergency | 3–6 months of expenses for crises | Highest |

| Essentials | Rent, food, utilities, transport | High |

| Equity | Investments, retirement, assets | Medium |

| Enjoyment | Travel, dining, hobbies | Lowest (only after others) |

Budgeting Apps: Tech as Your Financial Discipline Partner

Tracking your spending used to be tedious. Now, budgeting apps like Mint and Goodbudget make it automatic. These tools help you see exactly where your money goes, categorize expenses in real time, and keep your four buckets balanced. Technology isn’t just convenient—it’s your best friend for building discipline and avoiding emotional, impulsive decisions.

The Real American Dream: Wealth Is What You Keep

Forget the old American Dream of chasing status symbols and designer brands. That’s the American debt trap, not the dream. Wealth isn’t about what you buy, it’s about what you keep. Flashy spending on clothes, cars, or even homes before you’re financially stable is a recipe for disaster. Focus on building your emergency fund and investing in equity before you even think about luxury.

Credit Card Debt and Home Buying: Plan, Don’t Panic

Credit card debt is the silent killer of financial goals for millennials. With average U.S. credit card interest rates between 22–28%, carrying a balance can quickly spiral out of control. Don’t fall for the trap—wait, plan, and save before making big purchases. When it comes to buying a home, be strategic. My wife and I waited until we were financially ready, keeping our annual mortgage at just 22% of our annual expenses. This allowed us to stay comfortable and avoid the stress of over-leveraging ourselves.

Wealth isn't about what you buy, it's about what you keep.

Key Takeaways

- Emergency Savings Fund: 3–6 months of expenses is the minimum.

- Four-Bucket Budget: Emergency, Essentials, Equity, Enjoyment—fund in order.

- Budgeting Apps Mint, Goodbudget: Automate tracking and stay accountable.

- Credit Card Debt: Avoid carrying balances at 22–28% interest.

- Financial Goals Millennials: Build your buffer before investing or spending on status.

Cheat Code #5: Automation—Because Willpower is Overrated

If you’re tired of feeling like you need superhuman willpower to manage your money, you’re not alone. The truth is, the most successful people don’t rely on discipline—they rely on systems. Personal finance automation is the ultimate cheat code for Millennials who want to build wealth without the daily grind of decision fatigue. Automate everything: savings, investments, bill pay, and even your spending limits. The less you have to remember or manage, the more you achieve.

Automate Savings and Investments: Make Wealth-Building the Default

Let’s be honest—saving money is hard, especially when you have to make the choice every single month. That’s why the best financial literacy resources all agree: Automate savings and investment before your paycheck hits your hand. If you hate saving, this one move will make it effortless. Set up automatic transfers to your savings or investment accounts the moment your paycheck lands. This way, you pay your future self first, not last.

When I was in my 20s, I wish I had let technology take care of my finance.

I regret not automating my retirement contributions and investments sooner. Compound interest is magic, but it only works if you start early and stay consistent. Automating your savings and investments means you never miss an opportunity for your money to grow.

Automate Bill Payments: Eliminate Expensive Mistakes

Missed payments and late fees aren’t just annoying—they’re expensive and can tank your motivation. Set up automatic payments for everything: utilities, credit cards, subscriptions, rent. Automatic bill pay eliminates the risk of forgetting and protects your credit score over time. According to recent research, automating bill payments can increase your average credit score and reduce the risk of costly errors.

- Never miss a payment

- Avoid late fees

- Protect your credit score

Automate Your Spending Control: Guard Rails for Your Wallet

Impulse spending is one of the biggest threats to your financial goals. But you can use technology to put guard rails around your discretionary spending. Many banking apps now let you set up automatic spending limits, alerts, and even round-up features that funnel spare change into savings. These digital tools act as your financial safety net, helping you stay on track without constant vigilance.

- Set spending limits in your banking app

- Use alerts for large purchases

- Automate round-ups to savings or investments

Go Analog for Focus: The Power of Digital Detox

While automation frees up your mental bandwidth, it’s also important to occasionally unplug. Studies show that a one-week social media detox can boost attention span and cognitive function (2017 study). Use digital tools for your finances, but don’t be afraid to go analog—journaling, planning, or simply taking a break from screens can restore your critical thinking and stamina for deep work.

How Automation and Tech Tools Improve Financial Outcomes

| Automation Strategy | Benefit | Research/Data |

|---|---|---|

| Automated Savings/Investing Before Paycheck | Increases wealth outcomes, consistency | Automated contributions lead to higher savings rates (Source: Financial Literacy Resources) |

| Automatic Bill Pay | Eliminates late fees, boosts credit score | Reduces missed payments, increases average credit score over time |

| Digital Detox (1 week) | Improves cognitive function, focus | 2017 study: 1-week detox boosts attention span/cognition |

Key Takeaways for Personal Finance Automation

- Automate savings and investments—make wealth-building effortless.

- Automate bill payments—never pay a late fee again.

- Automate spending control—use tech to protect yourself from yourself.

Automate savings and investment before your paycheck hits your hand.

Learn from my mistakes: let technology handle your finances, and free up your willpower for things that matter most.

Cheat Code #6: The Power (and Peril) of Mentorship, Failure, and Humility

The Importance of Mentorship: Don’t Wait Until 40

If you want to shortcut your journey to financial freedom and career success, here’s the truth: Having a mentor is like having the ultimate cheat code for the game of life. Yet, most people—myself included—wait far too long to seek out real, invested mentors. I waited until I was 40 to get a mentor. Don’t make the same mistake. For years, I tried to navigate the career minefield blindfolded. I didn’t know what I was doing, and it showed. My progress was slow, my confidence shaky, and my network limited.

Everything changed when I found the right mentors. Within a decade of being mentored by one of the most inspiring CEOs I’ve ever met, I became a CEO myself. I worked alongside some of the most brilliant minds on the planet. Was that a coincidence? Not at all. Career Growth Mentorship is the difference between wandering in circles and accelerating straight to your goals.

Choosing the Right Mentor: Red Flags and Real Value

Not all mentorship is created equal. Beware of executive coaches who sell advice like a product. Authentic mentors are invested in your growth, not your wallet. If you want inspiration, skip the self-help fluff and check out Trillion Dollar Coach by Eric Schmidt, Jonathan Rosenberg, and Alan Eagle. It’s the story of Bill Campbell, who mentored Silicon Valley’s greatest leaders—not for a fee, but out of genuine belief in their potential. That’s the kind of Financial Advisor Guidance you want: real, supportive, and invested in your success.

Failure: Your Crash Course in Resilience

Let’s talk about the flipside of mentorship: failure. I’ve been fired not once, not twice, but three times in my career. Each time, it was brutal—no warning, no gentle letdown. Just, “We’re letting you go. We’ll send your stuff in boxes later.” Each period of unemployment lasted over six months. Every day felt like a struggle, and reaching out to my network or even friends was tough. I felt embarrassed and like a failure.

But here’s what I learned: Failure is not our tormentor, it’s our teacher. If you learn from it, every setback becomes a stepping stone. Those firings were catalysts. They forced me to adapt, to build resilience, and to seek out better opportunities. Overcoming Financial Challenges isn’t just about winning; it’s about learning from every shake-up and coming back stronger.

Success Is a Team Sport: Don’t Let Fear Hold You Back

Here’s another hard-won lesson: Success is a team sport. For years, fear was my biggest kryptonite. I was so afraid of rejection that I stayed stuck in mediocrity. I wasted years not asking for help, not reaching out, and not building the network I needed. Now, I embrace rejection. I know I’ll be turned down, and that’s okay. The sooner you get comfortable with a little embarrassment, the faster you’ll grow.

If you’re struggling to ask for help, remember: nobody builds wealth or a career alone. Your network, your mentors, and your willingness to learn from others are your greatest assets.

Wild Card Inspiration: Ed Sheeran’s Road to Stadiums

Still worried about rejection? Take a cue from Ed Sheeran. Every record label turned him down. He was told he was too ginger, too acoustic, too nerdy. He got booed off stage. But he kept showing up. Today, he sells out stadiums worldwide. A little embarrassment is a small price to pay for breakthrough success.

I waited until 40 to get a mentor. Don’t make the same mistake.

Having a mentor is like having the ultimate cheat code for the game of life.

- Career Growth Mentorship opens doors you can’t even see yet.

- Overcoming Financial Challenges is about learning from every setback.

- Real mentors and a strong network are your secret weapons—don’t go it alone.

Wild Cards: Ownership Mindset, Status Symbols, and The Analog Advantage

Let’s get real about Financial Mindset Millennials need to thrive: it’s not about chasing the next salary bump or collecting shiny status symbols. It’s about playing the long game, building true financial security, and owning your future in ways most people never even consider. If you want to break out of the paycheck-to-paycheck cycle and actually build wealth, you need to understand the wild cards that separate the top 1% from everyone else.

First, let’s talk about the difference between salary and equity. Salary is nice. It pays the bills, maybe lets you buy that new couch or take a decent vacation. But here’s the truth:

Salary buys you furniture, equity buys you future.The wealthy don’t chase paychecks—they chase equity. Why? Because equity is exponential. When you own a piece of something—a company, a property, even a small stake in a startup—you’re not just trading your time for money. You’re giving yourself a shot at unlimited upside. Sure, you might swing and miss nine times out of ten. I’ve had stock options in companies that flopped, and some that did okay, but didn’t move the needle. But the one time I hit it? That was a rainmaking event. It changed my life.

There’s another hidden benefit to equity: it forces you to think like an owner. Even if your slice is tiny, you start to see the bigger picture. You care about the company’s growth, the team’s performance, the market’s direction. That shift in mindset changes how you approach your work and your career. It’s the secret weapon for wealth building strategies—and for leadership. When you own, you act differently. You take calculated risks. You stop obsessing over titles, logos, and cars, and start chasing freedom and control. That’s the real status symbol: autonomy over your time and your choices.

But here’s the twist most people miss: your mindset is more important than any method or spreadsheet. The psychology of money, your confidence, and your ability to tune out the noise are what set you apart. Want a shortcut? Read The Psychology of Money by Morgan Housel or The Algebra of Wealth by Scott Galloway. These books will rewire how you think about risk, reward, and what actually matters.

Now, let’s talk about the analog advantage. We live in a world of constant distraction—doom scrolling, endless notifications, and digital noise that kills your critical thinking. In the 1970s, 40% of high school seniors read at least six books a year. Today, that number has flipped. Most people don’t read anything. But here’s the good news: even a one-week break from social media can improve your attention span and cognitive function. Deep reading and analog learning are rare assets in a distracted world. When you read real books, you engage with complex ideas, expand your vocabulary, and sharpen your focus.

Your ability to be focused will be your superpower.

So, what does this mean for Financial Security Millennials? It means you need to own your growth. Take risks. Ignore the pressure to keep up with status symbols. Build your focus muscle by going analog—read, think deeply, and invest in your own development. The top 1% aren’t just lucky; they play a different game. They chase equity, not salaries. They value freedom over flash. And they know that mindset always trumps method.

To wrap up, remember: the real cheat codes aren’t secret formulas or overnight hacks. They’re the wild cards—an ownership mindset, a rejection of empty status, and the analog advantage of deep focus. If you want to build lasting wealth and real financial security, these are your unfair advantages. Swing for equity, read real books, and never let anyone else define your value. That’s how you go from surviving to thriving—no BS required.

TL;DR: Key takeaways: Invest early (don't just save), treat careers and connections like compounding assets, automation beats willpower, build an emergency fund before anything fancy, learn from failure (and mentors), and don't buy the status symbol hype. Mix in critical thinking, ownership mindset, and actually asking for help—these are your real financial cheat codes.

Post a Comment